Pa 501 Form

Pa 501 Form

Filling out the PA 501 form can seem straightforward, but many make common mistakes that can lead to delays or complications. One frequent error occurs when individuals fail to enter the correct quarter and year at the top of the form. This information is crucial for accurate record-keeping and processing. Always double-check that you’ve selected the right quarter and entered the year correctly.

Another common mistake is neglecting to include the Employer Account ID or the Entity ID (Federal EIN). If you do not have an assigned number, it’s important to leave that section blank, rather than entering incorrect or placeholder information. This can confuse the processing department and lead to further issues down the line.

People often miscalculate the total amount of compensation subject to PA Withholding Tax. On Line 1, ensure that you enter the total compensation accurately. This is essential, as it affects the amount of tax withheld. If this figure is incorrect, it can lead to discrepancies that may require additional follow-up.

Line 2 requires the total amount of PA Withholding Tax. A mistake here is entering the amount of deposits instead of the actual tax withheld. It’s vital to report the correct figure to avoid penalties or audits. Remember, this line should reflect the tax that was withheld during the deposit period, not what you plan to deposit.

Another area where mistakes often occur is in Line 3, where you apply any credits from previous periods. Individuals may forget to include these credits or miscalculate them. This oversight can lead to paying more tax than necessary. Always review your previous filings to ensure you’re accurately applying any credits.

Interest due for late payments should be entered on Line 4. Many people overlook this line or forget to calculate the interest owed. If you are remitting after the due date, failing to include interest can result in additional penalties.

Signing the document is a crucial step that some individuals forget. Without a signature, the form is incomplete and may not be processed. Make sure to sign and date the form, and include your daytime telephone number and title. This information allows the department to contact you if there are any questions.

Mailing the deposit statement to the correct address is another common pitfall. Ensure that you send it to the PA Department of Revenue at the specified address. Sending it to the wrong location can cause significant delays in processing your payment.

Finally, many employers overlook the requirement to file a PA-W3 Reconciliation Return for each quarter. This form is necessary in addition to the PA 501. Failing to submit it can lead to issues with compliance and may result in penalties. Always remember to check that you have completed all required forms before submitting.

When completing the PA 501 form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of seven things to do and not do during this process.

Following these guidelines will help ensure that the PA 501 form is filled out correctly and submitted on time.

Pa 100 - The form can also be used to reactivate previously registered accounts.

To ensure a smooth establishment of your LLC, it is recommended to utilize resources like the PDF Document Service, which provides a comprehensive New York Operating Agreement template that can assist in defining the necessary management structure and operating procedures effectively.

Pennsylvania Nonresident Filing Requirements - An important step is to download the form onto your computer before filling it out.

Ebt Income Limit - Clients will receive specific notifications regarding the status of their submissions.

The PA-501 form is similar to the IRS Form 941, which is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Both forms require employers to provide information on wages paid and taxes withheld during a specific period. Employers must file Form 941 quarterly, similar to how the PA-501 is filed for Pennsylvania state taxes. Each form helps ensure compliance with federal and state tax laws, making it crucial for employers to accurately report their withholding amounts.

When engaging in property transactions, utilizing the correct documentation is critical. For instance, a thorough understanding of the necessary Deed paperwork can streamline the process significantly. To access the specific requirements and guidelines, please refer to this detailed California Deed form guide.

Another document that resembles the PA-501 is the IRS Form W-2. This form is issued to employees at the end of the year and summarizes the total wages earned and taxes withheld. Like the PA-501, the W-2 provides essential information for tax reporting purposes. Employers use both forms to ensure that the correct amounts are reported to the respective tax authorities. While the PA-501 focuses on quarterly withholding, the W-2 provides a comprehensive view of an employee's annual earnings and withholdings.

The PA-501 also shares similarities with the IRS Form 940, which is used to report annual Federal Unemployment Tax Act (FUTA) taxes. Both forms require employers to report amounts related to employee compensation and tax obligations. The PA-501 focuses on state income tax withholding, while Form 940 is concerned with unemployment taxes. Employers must file both forms to maintain compliance with different tax regulations, highlighting the importance of accurate reporting across various tax types.

Lastly, the PA-501 is akin to the state-specific Form W-3, which is the reconciliation of the W-2 forms submitted to the state. Just as the PA-501 summarizes the withholding for a quarter, the W-3 consolidates the information from all W-2 forms issued by an employer for the year. Both forms serve as a way for employers to report and reconcile tax information, ensuring that they meet their obligations to both state and federal tax authorities.

Completing the PA 501 form requires careful attention to detail. This form is essential for reporting income tax withheld from employee wages. Follow these steps to ensure accurate submission.

After submitting the PA 501 form, remember that all employers must also file a PA-W3 Reconciliation Return for each quarter. If you do not have a preprinted coupon, file a PA-W3R return as well. For any questions, contact the Employer Tax Division at (717) 783-1488.

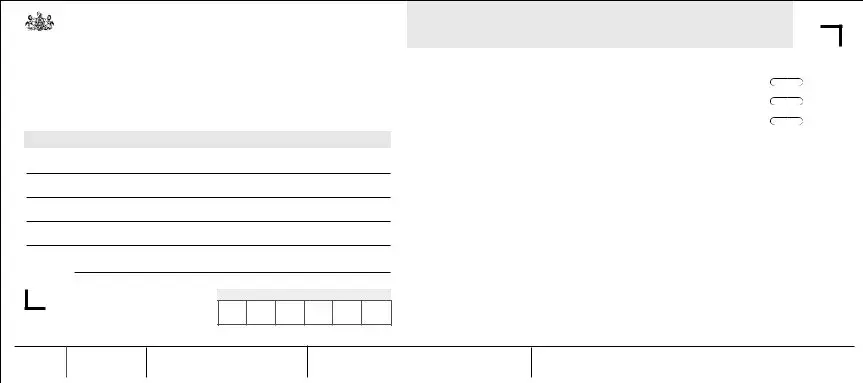

IN STRUCTIO N S FO R THE CO M PLETIO N O F FO RM PA - 5 0 1 R EM PLO YER DEPO SIT STATEM EN T O F IN CO M E TAX W ITHHELD

Enter the quarter (1st quarter YY01, 2nd quarter YY02, 3rd quarter YY03, and 4th quarter YY04), calendar year, the Employer Account ID (if none assigned, leave blank), Entity ID – Federal EIN (if none assigned, leave blank), quarter ending date (1st quarter 0331YYYY, 2nd quarter 0630YYYY, 3rd quarter 0930YYYY and 4th quar- ter 1231YYYY), date wages were first paid and payment frequency.

Enter the legal name, trade name and business mailing address as it should appear on future correspondence.

CO M PLETE LIN ES 1 THRO UGH 4

Line 1. Enter the total amount of compensation subject to PA Withholding Tax for the deposit period.

Line 2. Enter the total amount of PA Withholding Tax required to be withheld (or actually withheld, if greater) for the deposit period. (Enter tax withheld, not deposits)

Line 3. Enter the amount of credit from a previous period which is being applied to the amount withheld for the deposit period.

Line 4. Enter interest due for this payment if remitting after the due date.

Payment. Enter the amount of the payment being remitted for this deposit period.

Sign the document and enter the date, daytime telephone number and title.

Mail the deposit statement and payment to: PA Department of Revenue, Dept. 280401, Harrisburg, PA

Questions regarding the completion of this form can be directed to the Employer Tax Division at (717)

In addition to the

|

|

QUARTER |

|

|

|

YEAR |

|||||||||||||

PA DEPARTMENT OF REVENUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Y Y Q Q |

|

|

|

|

|

Y Y Y Y |

|||||||||||||||

|

|

|

EMPLOYER ACCOUNT ID |

|

|

ENTITY ID (EIN) |

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BUSINESS NAME AND ADDRESS

LEGAL NAME

TRADE NAME

BUSINESS MAILING ADDRESS

CITY, STATE, ZIP

DATE WAGES FIRST PAID

DEPARTMENT USE ONLY

EM PLO YER DEPO SIT STATEM EN T O F W ITHHO LDIN G TAX

Use Only When Employers Do Not Have Preprinted Coupons.

ALL EMPLOYERS MUST FILE A

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PAYMENT FREQUENCY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXPECTED QUARTERLY WITHHOLDING WILL BE: |

|

|

|

QUARTER ENDING DATE |

QUARTERLY |

||||||||||||||

|

|

|

LESS THAN $300 |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MONTHLY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MORE THAN $300 BUT LESS THAN $1,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

M M D D Y Y Y Y |

|||||||||||||||||

|

$1,000 OR GREATER |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

GROSS COMPENSATION |

|

|

|

|

|

|

▲ |

|

|

|

|

▲ |

|

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

PA WITHHOLDING TAX |

|

|

|

|

|

|

|

|

|

|

|

|

▲ |

|

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

LESS CREDITS |

|

|

|

|

|

|

|

|

|

|

|

|

▲ |

|

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4 |

PLUS INTEREST |

|

|

|

|

|

|

|

|

|

|

|

|

▲ |

|

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

PAYMENT $ |

|

|

|

|

▲ |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

● |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00021

DATE

DAYTIME TELEPHONE #

()

TITLE

SIGNATURE

PA DEPARTMENT OF REVENUE DEPT 280401 HARRISBURG PA

| Fact Name | Details |

|---|---|

| Form Purpose | The PA-501 form is used by employers to report income tax withheld from employees' wages. |

| Filing Frequency | Employers must file this form quarterly, depending on their withholding amounts. |

| Required Information | Employers must provide details such as compensation amounts, tax withheld, and any credits applied. |

| Submission Address | The completed form should be mailed to the PA Department of Revenue, Harrisburg, PA. |

| Governing Law | The PA-501 form is governed by Pennsylvania tax law regarding employer withholding requirements. |

| Contact Information | Questions about the form can be directed to the Employer Tax Division at (717) 783-1488. |

| Additional Requirements | Along with the PA-501, employers must also file a PA-W3 Reconciliation Return each quarter. |