Pa W3R Form

Pa W3R Form

Filling out the PA W3R form can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax filings. One frequent error is failing to include the correct Employer Account ID or Entity ID (EIN). These identifiers are crucial for the Pennsylvania Department of Revenue to process the return accurately. If you do not have an Employer Account ID, it's essential to leave that field blank rather than making assumptions about what to enter.

Another mistake involves the amount reported for tax withholding. Many individuals confuse the actual tax withheld with the deposits they have made. It's important to remember that the form requires the amount of tax that was actually withheld from employee wages, not the total deposits sent to the state. This distinction is vital for ensuring that your return reflects the correct figures.

In addition, some filers overlook the requirement to complete all lines from 1 to 5. Each line serves a specific purpose and provides necessary information to the tax authorities. Missing even one line can result in your form being returned for corrections, which can delay processing and potentially lead to penalties. Always double-check that every line is filled out accurately before submitting.

Finally, many people forget to sign and date their return. This step is often seen as a formality, but it is legally required. Without a signature, the return may not be considered valid, and the Department of Revenue might not process it. Make sure to include your daytime telephone number and title as well, as this information can be helpful if the tax department needs to reach you for any reason.

When filling out the PA W3R form, it's essential to approach the task with care and attention to detail. Here are some important dos and don'ts to consider:

By following these guidelines, you can ensure that your PA W3R form is completed correctly and submitted on time. This will help avoid any potential issues with your tax obligations.

Ebt Income Limit - The PA564 form is a semiannual reporting document for public assistance recipients in Pennsylvania.

To navigate the complexities of property transfers, understanding the necessary documentation is crucial. Our guide on how to complete a Deed form correctly can ease the process significantly. Learn more about the requirements and procedures involved by accessing the information through the following link: thorough guide to the Deed form.

Pennsylvania Senior Citizen Id Card - Sections A through F of the DL-80 must be filled out completely to ensure proper processing.

The IRS Form 941 is a document that employers in the United States use to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Similar to the PA W3R form, it requires employers to report the total amount of wages paid and the taxes withheld during a specific quarter. Both forms serve the purpose of reconciling the amounts withheld from employees with what has been reported to the government, ensuring accurate tax collection. Employers must file this form quarterly, just like the PA W3R, making it essential for maintaining compliance with federal tax laws.

The IRS Form W-2 is another important document for employers. It reports an employee's annual wages and the taxes withheld from their paychecks throughout the year. Like the PA W3R, it provides a summary of compensation and withholding, but it is focused on individual employees rather than the total for the employer. Both forms require accurate reporting to ensure that taxes are correctly calculated and remitted. The W-2 form is issued to employees at the end of the year, while the PA W3R is a quarterly reconciliation, highlighting the continuous nature of tax reporting.

For those interested in the specifics of forming a limited liability company, acquiring the PDF Document Service can be invaluable, as it offers a comprehensive guide to understanding the New York Operating Agreement, which is essential for clearly defining membership roles and preventing potential conflicts.

The Pennsylvania Form REV-419 is similar in that it is used to report and reconcile the state income tax withheld from employees. This form is specifically tailored for Pennsylvania employers, similar to the PA W3R. Both documents require detailed information about the amounts withheld and the employer's identification. They help ensure that the state receives the correct amount of tax revenue. Employers must file this form periodically, aligning it with the quarterly filing requirements of the PA W3R.

The IRS Form 945 is used to report federal income tax withheld from non-payroll payments, such as pensions and annuities. While it serves a different purpose than the PA W3R, both forms require accurate reporting of withheld taxes. Employers who make non-payroll payments must ensure compliance with federal tax laws, just as they do with employee payroll taxes. Both forms emphasize the importance of reporting and remitting the correct amounts to the government.

The IRS Form 1099-MISC is used to report payments made to independent contractors and other non-employees. Similar to the PA W3R, it requires the reporting of amounts paid and the taxes withheld. However, the 1099-MISC focuses on payments outside of traditional employment, while the PA W3R deals specifically with employee wages. Both forms are crucial for ensuring that all income is reported and that appropriate taxes are paid, highlighting the broader scope of tax compliance.

The IRS Form 1040 is the individual income tax return form that taxpayers use to report their annual income. While it is different in purpose from the PA W3R, both forms ultimately contribute to the same goal: accurate tax reporting. The PA W3R helps employers report withholding amounts, while the 1040 allows individuals to report their total income and taxes owed. Both forms require careful attention to detail and accurate reporting to avoid penalties and ensure compliance with tax laws.

Completing the PA W3R form is an essential task for employers in Pennsylvania who need to report income tax withheld from employees. This form helps ensure that the correct amounts are reported and paid to the state. Below are the steps to fill out the form accurately.

If you have any questions about filling out this form, you can contact the Employer Tax Division at (717) 783-1488 for assistance.

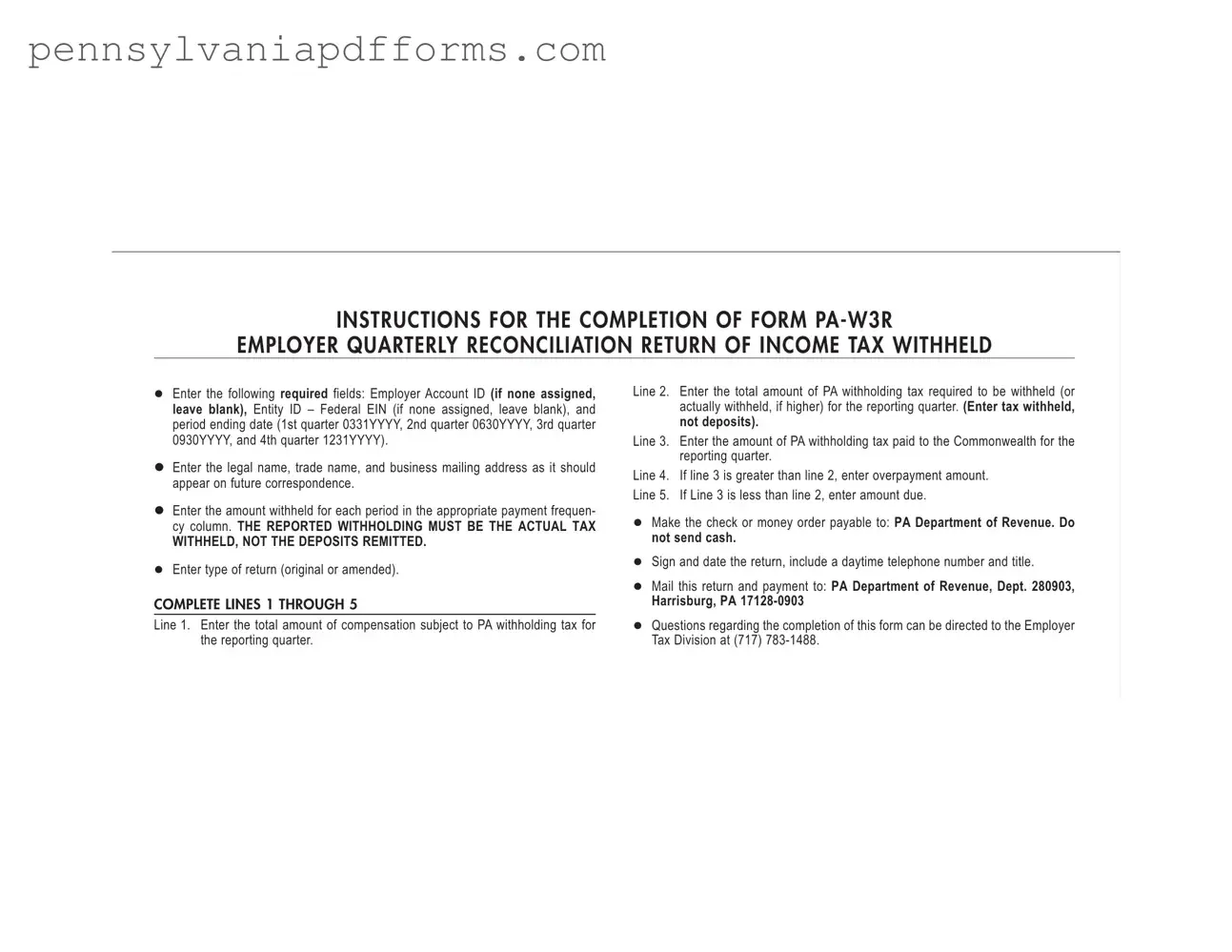

INSTRUCTIONS FOR THE COMPLETION OF FORM

EMPLOYER QUARTERLY RECONCILIATION RETURN OF INCOME TAX WITHHELD

Enter the following required fields: Employer Account ID (if none assigned, leave blank), Entity ID – Federal EIN (if none assigned, leave blank), and period ending date (1st quarter 0331YYYY, 2nd quarter 0630YYYY, 3rd quarter 0930YYYY, and 4th quarter 1231YYYY).

Enter the legal name, trade name, and business mailing address as it should appear on future correspondence.

Enter the amount withheld for each period in the appropriate payment frequen- cy column. THE REPORTED WITHHOLDING MUST BE THE ACTUAL TAX

WITHHELD, NOT THE DEPOSITS REMITTED.

Enter type of return (original or amended).

COMPLETE LINES 1 THROUGH 5

Line 1. Enter the total amount of compensation subject to PA withholding tax for the reporting quarter.

Line 2. Enter the total amount of PA withholding tax required to be withheld (or actually withheld, if higher) for the reporting quarter. (Enter tax withheld, not deposits).

Line 3. Enter the amount of PA withholding tax paid to the Commonwealth for the reporting quarter.

Line 4. If line 3 is greater than line 2, enter overpayment amount. Line 5. If Line 3 is less than line 2, enter amount due.

Make the check or money order payable to: PA Department of Revenue. Do not send cash.

Sign and date the return, include a daytime telephone number and title.

Mail this return and payment to: PA Department of Revenue, Dept. 280903,

Harrisburg, PA

Questions regarding the completion of this form can be directed to the Employer Tax Division at (717)

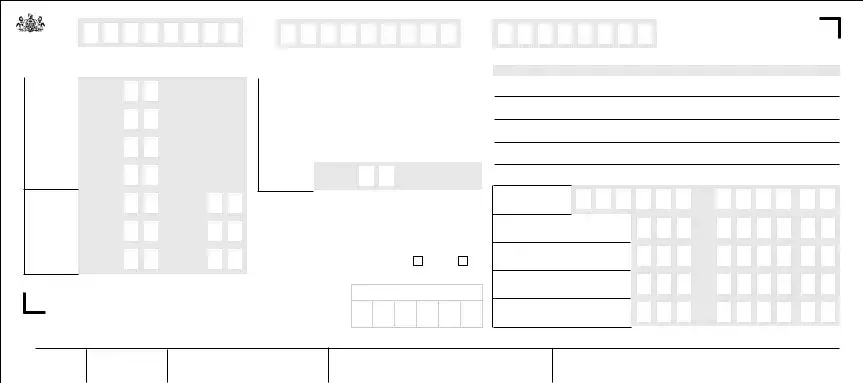

EMPLOYER ACCOUNT ID |

ENTITY ID (EIN) |

PERIOD ENDING DATE |

PA DEPARTMENT

OF REVENUE

PERIOD |

|

|

|

|

SEMI MONTHLY |

|

|

|

|

|

|||

|

|

|

AMOUNTS WITHHELD |

||||||||||

|

|

|

|

||||||||||

1ST HALF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1ST MONTH |

|

|

|

|

▲ |

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2ND HALF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1ST MONTH |

|

|

|

|

▲ |

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1ST HALF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2ND MONTH |

|

|

|

|

▲ |

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2ND HALF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2ND MONTH |

|

|

|

|

▲ |

|

|

|

● |

|

|

|

|

PERIOD |

|

|

|

|

|

MONTHLY |

|

|

|

|

|

||||

|

|

|

AMOUNTS WITHHELD |

||||||||||||

|

|

|

|

||||||||||||

1ST |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MONTH |

|

|

|

|

|

▲ |

|

|

|

|

● |

|

|

|

|

2ND |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MONTH |

|

|

|

|

|

▲ |

|

|

|

|

● |

|

|

|

|

3RD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MONTH |

|

|

|

|

|

▲ |

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

|

|

|

|

|

▲ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(Enter on Line 2) |

|

|

|

|

|

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

M M D D Y Y Y Y

BUSINESS NAME AND ADDRESS

LEGAL NAME

TRADE NAME

BUSINESS MAILING ADDRESS

CITY, STATE, ZIP

▼ LINES 1 – 5 MUST BE COMPLETED. ▼

1ST HALF |

|

|

|

|

|

|

|

|

|

|

|

3RD MONTH |

|

|

|

|

▲ |

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

2ND HALF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3RD MONTH |

|

|

|

|

▲ |

|

|

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

|

|

|

|

▲ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(Enter on Line 2) |

|

|

|

|

|

|

|

|

● |

||

QUARTERLY AMOUNT WITHHELD. |

||||

ENTER ON LINE 2 ONLY ➡ |

|

|

|

|

|

|

|

|

|

TYPE OF RETURN |

ORIGINAL |

AMENDED |

||

Original or amended. Check block. ➡ |

|

|

|

|

1. TOTAL COMPEN- |

|

SATION SUBJECT |

▲ |

TO PA TAX |

2. TOTAL PA WITHHOLDING TAX |

3. TOTAL DEPOSITS FOR QUARTER |

(Including verified overpayments) |

▲  ▲

▲

▲  ▲

▲

▲  ▲

▲

●

●

●

MAILCOMPLETED

DEPT. 280903 HARRISBURG,

DEPARTMENT USE ONLY

4. OVERPAYMENT |

(If Line 3 is greater than Line 2) |

5. TAX DUE/PAYMENT |

$ |

(If Line 3 is less than Line 2) |

▲  ▲

▲

▲  ▲

▲

●

●

I certify that this return is to the best of my knowledge, information and belief, a full, true and correct disclosure of all tax collected or incurred during the period indicated on this return.

00019

DATE

DAYTIME TELEPHONE # |

EXT. TITLE |

()

SIGNATURE

PA DEPARTMENT OF REVENUE DEPT 280903

HARRISBURG PA

| Fact Name | Description |

|---|---|

| Purpose | The PA W3R form is used for the quarterly reconciliation of income tax withheld by employers in Pennsylvania. |

| Required Information | Employers must provide their Employer Account ID, Federal EIN, and the period ending date, along with the legal name and business mailing address. |

| Tax Reporting | Employers must report the actual tax withheld, not the deposits remitted, for the reporting quarter. |

| Payment Instructions | Checks or money orders should be made payable to the PA Department of Revenue. Cash is not accepted. |

| Contact Information | Questions can be directed to the Employer Tax Division at (717) 783-1488 for assistance with the form. |

| Governing Law | The PA W3R form is governed by Pennsylvania state tax laws regarding income tax withholding. |