Pennsylvania Form

Pennsylvania Form

Filling out the Pennsylvania form can be a straightforward process, but several common mistakes can lead to complications. One frequent error is failing to provide complete information. Each section of the form must be filled out accurately. Missing details, such as the tax period or the specific type of petition, can result in delays or even dismissal of the appeal.

Another mistake often made is not signing the petition. All petitions must be signed by the petitioner or an authorized representative. If the form is signed only by a representative, a written authorization must accompany it. Omitting a signature can lead to the petition being considered incomplete.

Many individuals also overlook the importance of including the correct Social Security Number (SSN) or Employer Identification Number (EIN). For individual, estate, and partnership appeals, the SSN is required. Providing an incorrect number can hinder the processing of the appeal and create unnecessary complications.

Another common oversight is not attaching the necessary documentation. The form requests that a copy of the notice being appealed is included. Failing to attach this document can result in the Board of Appeals being unable to review the case properly.

In addition, some people do not clearly articulate the issues involved in their appeal. It is essential to itemize the issues and provide a detailed explanation of why relief should be granted. A vague or unclear description can lead to misunderstandings and may affect the outcome of the appeal.

Lastly, individuals sometimes neglect to choose their preferred method of communication. The form allows for correspondence to be sent via U.S. mail or email. Not indicating a preference can lead to delays in receiving important information regarding the appeal.

When filling out the Pennsylvania form, it’s essential to follow specific guidelines to ensure your petition is processed smoothly. Here’s a list of things you should and shouldn’t do:

The Pennsylvania Seller Property Disclosure Requires the Disclosure of - Even if a seller indicates 'no' issues, a professional inspection may reveal hidden problems.

The New York Trailer Bill of Sale serves as a vital tool for anyone looking to transfer ownership of a trailer, detailing key elements like the buyer and seller's information, the description of the trailer, and the agreed sale price. To further assist in navigating the complexities of this process, resources such as PDF Document Service can provide templates and guidance to ensure all necessary information is accurately captured.

Ebt Income Limit - The form ensures updated data is utilized for assistance calculations.

Pa501 - It is important to keep a copy of the completed form for your records.

The Pennsylvania Board of Appeals petition form shares similarities with the IRS Form 843, which is used to claim a refund or request an abatement of certain taxes. Both documents require detailed information about the taxpayer, including their identification and tax account numbers. They also necessitate a clear statement of the reason for the request, whether it is for a refund or an abatement. In both cases, the taxpayer must certify the accuracy of the information provided and may need to attach supporting documentation to substantiate their claims.

Another comparable document is the California Board of Equalization Petition for Redetermination, which allows taxpayers to contest tax assessments. Like the Pennsylvania form, this document requires taxpayers to specify the type of tax being contested and the period in question. Both forms also ask for a description of the issues involved and provide a space for taxpayers to outline their arguments. The need for signatures and certifications of truthfulness is a common feature, ensuring accountability in the claims made.

The New York State Tax Appeals Tribunal’s Petition for Review form is also similar. It allows taxpayers to appeal decisions made by the Department of Taxation and Finance. This form, like the Pennsylvania petition, requires the taxpayer to provide their identification details, the tax type, and the assessment amount. Both forms emphasize the importance of a detailed explanation of the reasons for the appeal and require the taxpayer's signature to validate the petition.

In Texas, the Notice of Appeal form serves a similar purpose. It allows taxpayers to challenge property tax appraisals. Much like the Pennsylvania form, it requires the appellant to provide relevant identification information and specifics about the contested assessment. Both documents emphasize the need for a clear statement of the grounds for the appeal and the requirement for signatures to confirm the authenticity of the submissions.

The Florida Department of Revenue's Petition for Administrative Hearing is another document that resembles the Pennsylvania form. This petition is used to contest tax assessments or denials. Both forms require the taxpayer to identify the tax type and provide a thorough explanation of the issues being appealed. Additionally, they necessitate signatures from the petitioner or their authorized representative, underscoring the importance of accountability in the appeals process.

In the realm of rental agreements, it is essential to have clear documentation to avoid misunderstandings, much like the Ohio Residential Lease Agreement form, which stipulates the responsibilities and rights of landlords and tenants. This form serves as a valuable reference for anyone looking to navigate the complexities of property rental. For further insights into the specifics of such agreements, you can explore https://topformsonline.com/ohio-residential-lease-agreement/.

The Illinois Department of Revenue’s Request for Hearing form is also similar. It allows taxpayers to request a hearing on tax assessments or denials. Both forms require the taxpayer to provide identification and details about the tax period in question. They also demand a concise explanation of the issues involved and require signatures to affirm the accuracy of the information provided.

Furthermore, the Massachusetts Appellate Tax Board Petition form mirrors the Pennsylvania form. This document is used to appeal property tax assessments. Like the Pennsylvania petition, it requires the taxpayer to provide their identification and specific details about the contested assessment. Both forms emphasize the necessity of a clear statement of the reasons for the appeal and the requirement for signatures to ensure the validity of the claims made.

Lastly, the Ohio Board of Tax Appeals form for filing a notice of appeal is similar in nature. This document is used to contest various tax assessments. Both the Ohio form and the Pennsylvania petition require the taxpayer to provide identification details, the type of tax involved, and a comprehensive explanation of the appeal's basis. The need for signatures to certify the truthfulness of the information is a common requirement in both documents, reinforcing the importance of integrity in the appeals process.

Filling out the Pennsylvania Board of Appeals petition form requires careful attention to detail. This process involves providing specific information related to your tax appeal. Following these steps will help ensure that your petition is complete and submitted correctly.

After completing the form, remember to attach a copy of the notice being appealed. Petitions can be submitted online or by mail, with online submissions preferred for immediate confirmation. Ensure all required information is included to avoid dismissal of your appeal.

(BA+)

(BA+)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

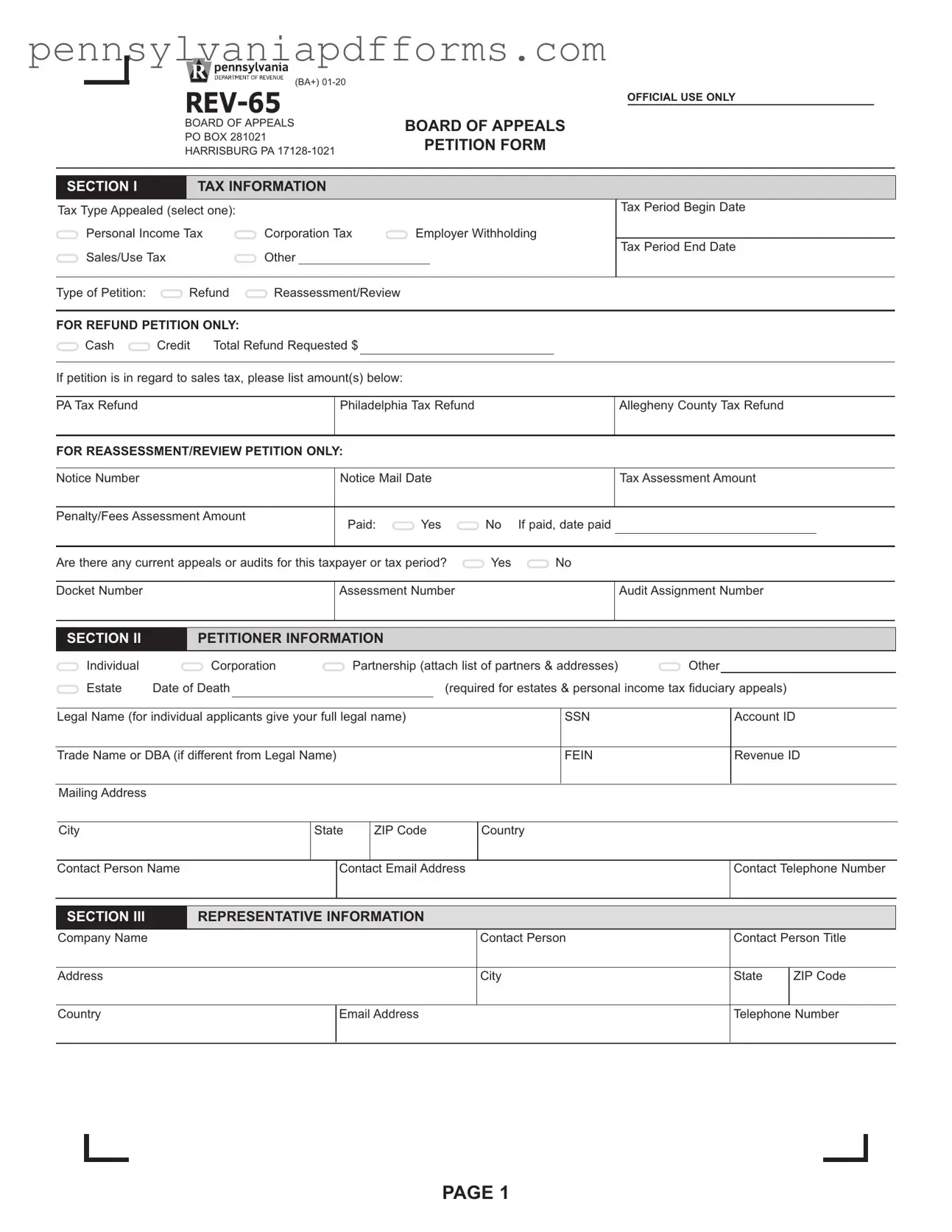

Tax Type Appealed (select one): |

|

|

|

|

|

|

|

|

|

Tax Period Begin Date |

||||

|

|

|

|

|

|

|

|

|

|

|

||||

Personal Income Tax |

|

Corporation Tax |

Employer Withholding |

|

|

|||||||||

Sales/Use Tax |

|

Other |

|

|

|

|

|

|

Tax Period End Date |

|||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Type of Petition: |

|

Refund |

Reassessment/Review |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash |

Credit |

Total Refund Requested $ |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If petition is in regard to sales tax, please list amount(s) below: |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

PATax Refund |

|

|

|

|

|

Philadelphia Tax Refund |

|

|

|

Allegheny County Tax Refund |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Notice Number |

|

|

|

|

|

Notice Mail Date |

|

|

|

Tax Assessment Amount |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Penalty/Fees Assessment Amount |

|

|

Paid: |

Yes |

No |

If paid, date paid |

||||||||

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Are there any current appeals or audits for this taxpayer or tax period? |

Yes |

|

No |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

Docket Number |

|

|

|

|

|

Assessment Number |

|

|

|

Audit Assignment Number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Individual |

Corporation |

|

|

Partnership (attach list of partners & addresses) |

Other |

|

||||||

Estate |

Date of Death |

|

|

|

|

(required for estates & personal income tax fiduciary appeals) |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal Name (for individual applicants give your full legal name) |

|

|

SSN |

|

|

Account ID |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade Name or DBA (if different from Legal Name) |

|

|

|

|

FEIN |

|

|

Revenue ID |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

|

|

State |

|

ZIP Code |

|

Country |

|

|

|

||

|

|

|

|

|

|

|

|

|

||||

Contact Person Name |

|

Contact Email Address |

|

|

Contact Telephone Number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

V

V

Company Name

Address

Country

Contact Person |

Contact Person Title |

||

City |

State |

|

ZIP Code |

|

|||

|

|

|

|

Email Address |

Telephone Number |

||

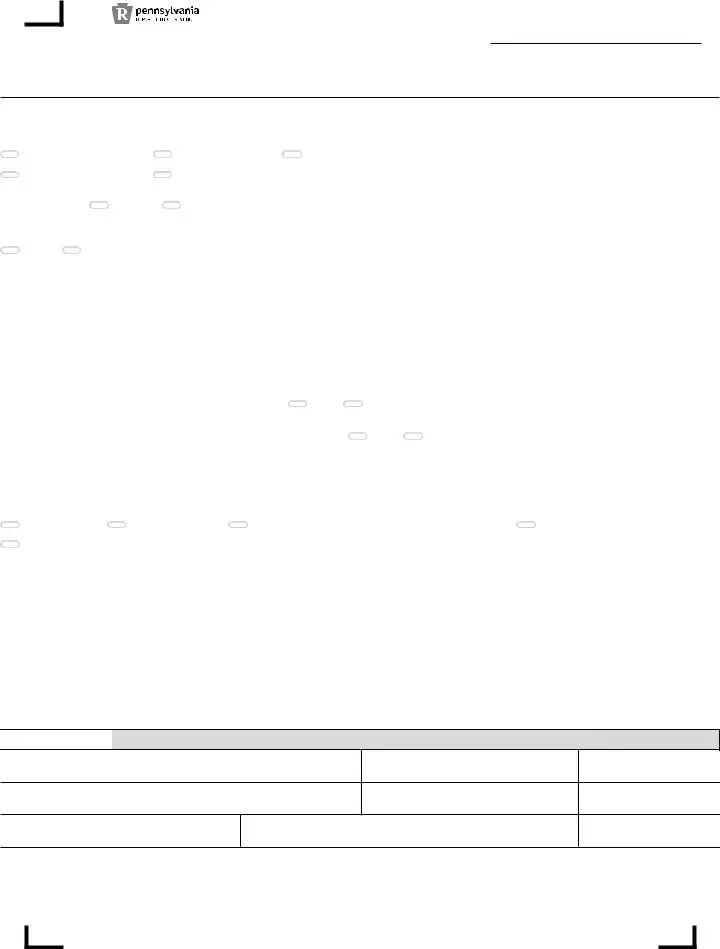

V

Hearing Requested |

No Hearing Requested. Please decide on basis of the petition and record. |

|||

This case to be held pending action on the same issue(s). Case Number |

|

Court Citation Number |

||

|

|

|

|

|

V

If you elect to receive communications via email, you are authorizing the Board ofAppeals to send correspondence, including the final Decision & Order, via email.

Send Correspondence to (select one): |

Petitioner |

Representative |

Send Correspondence via (select one): |

U.S. Mail |

|

Send Decision and Order via (select one): |

U.S. Mail |

V

Itemize the issue(s) involved. What is the subject of appeal? Attach a separate sheet if more space is required.

V

All petitions must be signed by the petitioner or authorized representative. If signed only by an authorized representative, written authorization must accompany the petition. If the petitioner is a corporation, a corporate officer must sign.

Under penalties prescribed by law, I hereby certify this petition has been examined by me, and to the best of my knowledge, information and belief, the facts contained in the petition are true, correct and complete and the petition is not made for the purpose of delay. Also, if this is a petition for refund, I certify that the refund requested has not been granted in an audit report, nor has it been included in any other petition for refund.

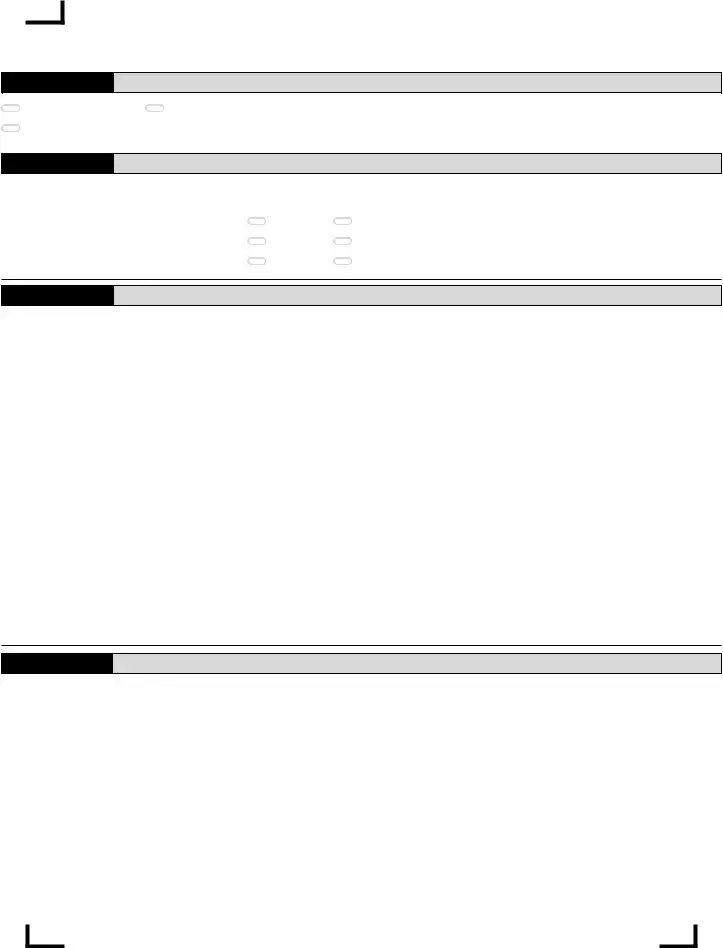

Petitioner’s Name |

Petitioner’s Signature |

Petitioner’s Title |

Date |

|

|

|

|

Representative’s Name |

Representative’s Signature |

Representative’s Title |

Date |

|

|

|

|

Please type or print neatly in blue or black ink.Attach acopy of the notice being appealed.

Petitions should be sent directly to the Board of Appeals online or by mail. The preferred method of filing is online because this method provides a confirmation number. Online petitions are filed through the Board of Appeals

website at rdppssttpus .The mailing address for the Board ofAppeals is:

-

Petition is considered filed as of the postmark date. Meter dates or any other mark (except the USPS postmark) is not recognized. Failure to include any required information may result in a dismissal of your appeal.

The Board of Appeals will consider compromises of assessment and refund appeals. If you wish to propose a compromise, please complete and submit a Request for Compromise

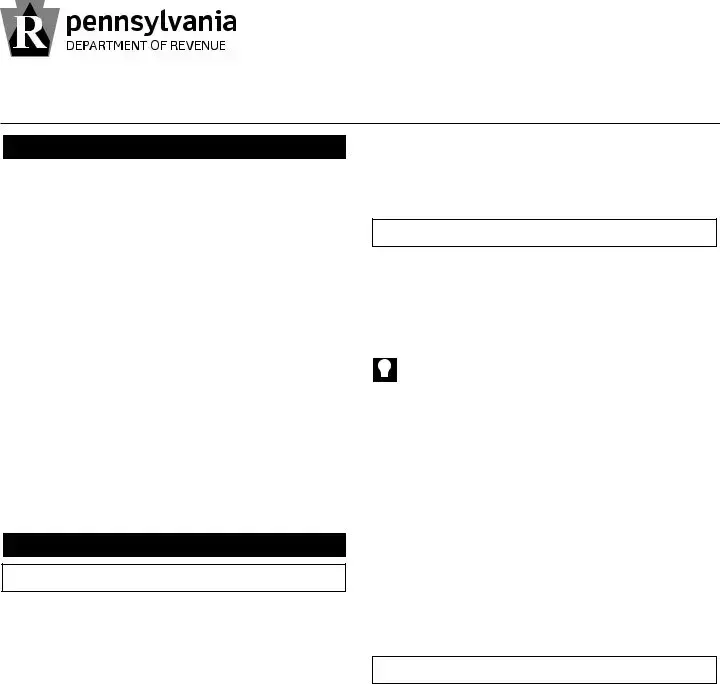

SECTION I

Fillintheovalforthetaxtypebeingappealed.Administrative Appeals of Record such as revocation of a lottery license can be identified in Other.

Please clearly identify the tax period being appealed.

Fillinonlyoneovalforthetypeofpetition.Donotmarkboth.

INSTRUCTIONS FOR

Board of Appeals Petition Form

If there are any current appeals or audit for this taxpayer or tax period, provide docket number, assessment number and/or audit assignment number. This section is applicable topetitionsforrefundandpetitionsforreassessment/review.

SECTION II

Social Security number is required for Individual, Estate and Partnership appeals. Include Social Security number for each partner when providing list of partner names and addresses.

The department is authorized under federal  law, 42 U.S.C. § 405 (c), to use your Social Security number in administering state tax law.The department uses your Social Security number to establish your identity and to process your appeal.

law, 42 U.S.C. § 405 (c), to use your Social Security number in administering state tax law.The department uses your Social Security number to establish your identity and to process your appeal.

Account ID Number is the number used to identify the tax account being appealed. Examples include the Sales Tax License Number, the Corporate Box Number, Estate File Number or Control Number.

FederalEmployerIdentificationNumberisissuedbytheIRS to business entities. Complete this number if one has been assigned to you.

Departmental issued number assigned to each business entity with a filing requirement in PA.

SECTION III

V

Representation by an attorney, CPA or other person is not required. Complete representative information only if Petitioner is represented by another person.

|

SECTION IV |

|

|

Provide refund form and amount requested. If the refund |

|

|

|

|

|

||

requested is for sales tax, provide requested amounts for |

Hearings,ifrequested,areheldinHarrisburg.Petitionermay |

||

PA tax refund. If applicable, provide amounts for |

|||

Philadelphia tax refund orAllegheny County tax refund. |

request a phone conference in lieu of a hearing. It is at the |

||

Board’s discretion whether to grant this request. |

|||

|

|||

Provide notice number, notice mail date, tax assessment |

SECTION V |

|

|

amount, and penalty/fees assessment amount. If the tax |

|

|

|

|

|

|

|

assessment amount and penalty/fees assessment amount |

|

|

|

have been paid in full, provide date paid. |

Please select desired method of correspondence. |

|

|

|

|

|

|

rvupv |

- |

1 |

|

Communication, including the board’s final  decision and order, may be transmitted to you or your representative via email, should you elect the email option. If you elect to receive communications via email, you and your representatives assume the responsibility for the confidentiality of the information contained in emails sent to and from the Board ofAppeals. The commonwealth will not be held liable for the disclosure of any confidential information sent via email.

decision and order, may be transmitted to you or your representative via email, should you elect the email option. If you elect to receive communications via email, you and your representatives assume the responsibility for the confidentiality of the information contained in emails sent to and from the Board ofAppeals. The commonwealth will not be held liable for the disclosure of any confidential information sent via email.

SECTION VI

Briefly state the issue(s) involved and explain in detail why relief should be granted.Additional pages may be attached, if necessary.

Any required appeal schedule should be submitted with the petition or within 30 days of the date that the petition is filed. Any evidence in support of the petition may be submitted with the petition but no later than 60 days from the date that the petition is filed.

SECTION VII

All petitions must be signed by the Petitioner and/or Authorized Representative. A Power of Attorney

2 - |

rvupv |

| Fact Name | Details |

|---|---|

| Form Title | REV-65 Board of Appeals Petition Form |

| Governing Law | Pennsylvania Tax Code, 72 P.S. § 7301 et seq. |

| Filing Method | Petitions can be filed online or via mail. Online filing is preferred. |

| Required Information | Petitions must include the notice being appealed and all relevant details. |

| Signature Requirement | Petitions must be signed by the petitioner or an authorized representative. |

| Refund Request | Refund petitions must specify the amount and type of tax being appealed. |

| Email Communication | Petitioners may opt to receive communications via email, assuming confidentiality. |

| Submission Deadline | Petitions must be filed by the postmark date; late submissions may be dismissed. |