Pennsylvania Petition Form

Pennsylvania Petition Form

Filling out the Pennsylvania Petition form can be a straightforward process, but many people make common mistakes that can delay their petitions or lead to rejection. One major mistake is failing to include the Board of Appeals Docket Number. This number is crucial for identifying your case. If you have it, make sure to write it down. If you don’t, it’s best to check with the Board of Appeals before submitting your petition.

Another frequent error is not providing complete information. Every section of the form must be filled out accurately. If the petitioner is an organization rather than an individual, including a contact person is essential. Omitting details can cause confusion and might result in a request for additional information, slowing down the process.

Some people forget to indicate if they are being represented by someone else. If you plan to have a representative, you need to fill out that section. All correspondence will then go to your representative instead of you. Missing this step can lead to miscommunication and delays.

When it comes to the tax information, ensure that you include the tax amount you are appealing. It's important to check one of the boxes indicating the type of petition. This clarity helps the Board understand your request better and can expedite the process.

Another common oversight is regarding hearings. If you wish to request a hearing, you need to indicate that on the form. If you prefer not to have a hearing, make sure to check the appropriate box. Not specifying your preference can lead to unnecessary delays.

Providing a signature is non-negotiable. All petitions must be signed by either the petitioner or an authorized representative. Failing to sign the form will result in automatic rejection, so double-check this before submitting.

Lastly, many people neglect to attach necessary supporting documents. The petition should include all pertinent facts, calculations, and evidence. If you are appealing a refund, proof of payment is essential. Not including these documents can lead to your petition being dismissed or delayed. Always remember to review your submission before sending it off.

When filling out the Pennsylvania Petition form, it’s important to be thorough and careful. Here are ten things you should and shouldn’t do to ensure your petition is processed smoothly.

By following these guidelines, you can help ensure that your petition is complete and stands the best chance of being favorably considered.

Pa W-2 Form - Taxpayers must complete Section I with details from federal Forms W-2 received from employers.

To further clarify the obligations and protections afforded to both landlords and tenants, reviewing the Ohio Residential Lease Agreement form is essential, and can be conveniently accessed at https://topformsonline.com/ohio-residential-lease-agreement/, which provides detailed information on the necessary terms and conditions for a successful rental relationship in Ohio.

Register Vehicle in Pa - Section E must always be filled for registration plate replacements.

The Pennsylvania Petition form shares similarities with the IRS Form 843, which is used to claim a refund or request an abatement of certain taxes. Both documents require the petitioner to provide specific details about the tax issue at hand, including the type of tax and the amount in question. Like the Pennsylvania Petition, the IRS Form 843 necessitates supporting documentation to substantiate the claim, emphasizing the importance of thorough evidence submission.

Another comparable document is the California Board of Equalization Petition for Redetermination. This form is utilized to contest tax assessments and includes sections for detailing the reasons for the appeal. Both forms require the petitioner to state their case clearly and provide relevant facts, ensuring that the reviewing authority has sufficient information to make an informed decision.

The New York State Petition for Administrative Review is also similar in nature. It is used to challenge decisions made by the Department of Taxation and Finance. Both forms require a clear statement of the issues being contested and the basis for the appeal. Each petition must be signed by the petitioner or an authorized representative, reflecting the necessity of accountability in the submission process.

The Texas Comptroller’s Office has a similar form, the Request for Hearing on Tax Matters. This document allows taxpayers to appeal decisions regarding tax assessments. Like the Pennsylvania Petition, it requires detailed information about the taxpayer, the tax type, and the amount being disputed. The importance of timely submission and adherence to procedural rules is a common theme across both forms.

Understanding the various forms used in administrative processes can lead to more effective communication and resolution. For example, the Ohio Lease Agreement form, like the Pennsylvania Petition, is designed to clearly outline terms and responsibilities, helping both parties avoid potential misunderstandings. Those interested in this agreement can refer to the PDF Document Service for a comprehensive template that ensures all necessary details are included, promoting a smoother renting experience.

The Florida Department of Revenue also utilizes a Petition for Review form. This document is employed to contest tax assessments or denials of refunds. Both the Florida and Pennsylvania petitions require the inclusion of supporting documentation and a clear explanation of the relief sought. The structured format helps ensure that all necessary information is presented for review.

In Illinois, the Department of Revenue offers a Petition for Adjustment of Tax. This form serves a similar purpose, allowing taxpayers to dispute tax liabilities. Both forms require the petitioner to outline the reasons for their appeal and provide evidence to support their claims. The procedural requirements, including deadlines for submission, are critical to both processes.

The Massachusetts Department of Revenue has a comparable document known as the Application for Abatement. This form is used to request a reduction in property tax assessments. Similar to the Pennsylvania Petition, it requires detailed information about the taxpayer and the tax issue. The emphasis on submitting supporting documents is a shared characteristic, highlighting the need for thoroughness in tax-related appeals.

The Virginia Department of Taxation utilizes a Request for Refund form, which allows taxpayers to seek refunds for overpayments. This document parallels the Pennsylvania Petition in that it requires a clear statement of the refund request and supporting evidence. Both forms aim to facilitate a fair review process by providing a structured approach to presenting tax disputes.

Lastly, the Ohio Department of Taxation offers a Tax Appeal form, which is used to contest tax assessments. Similar to the Pennsylvania Petition, it necessitates a detailed explanation of the reasons for the appeal and the desired outcome. Both forms underscore the importance of clarity and completeness in presenting one’s case to the relevant authorities.

After completing the Pennsylvania Petition form, you will submit it to the Board of Finance and Revenue. Ensure that all necessary information and supporting documents are included. You may also need to communicate with the Department of Revenue regarding your submission. Follow these steps carefully to ensure your petition is filed correctly.

Once you have completed these steps, submit your petition either electronically or by mail. Ensure you keep a copy of everything you send for your records.

Board of Finance & Revenue

General Instructions

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

AN E |

A |

N |

|

|

|

|

|

N |

||||

|

|

|

I |

|

|

|

||

|

|

|

F |

|

|

|

|

D |

|

|

O |

F |

|

|

|

|

R |

|

|

|

|

|

|

|

V |

|

|

|

|

|

|

|

|

|

E |

R |

D |

|

|

|

|

|

|

E |

A |

|

|

|

|

|

|

|

N |

O |

|

|

|

|

|

|

|

U |

B |

|

|

|

|

|

|

|

E |

|

|

P |

|

|

|

|

IA |

|

|

|

|

E |

N |

|

|

|

|

|

|

|

|

|

|

N |

||

|

|

|

|

|

NS YLVA |

|||

This Petition Form should be used to petition to the Board of Finance and Revenue for:

•Review of decisions of the Board of Appeals.

•Refund of monies paid to an agency of the Commonwealth, other than the Department of Revenue, to which the Commonwealth is neither rightfully nor equitably entitled.

Any evidence in support of the petition should be submitted with the petition or within 60 days from the date the petition is iled.

Petitioner and the Department of Revenue must provide a copy of each submission provided to the Board to the other party. The preferred method is electronic submission (10MB limit). Submissions may be mailed/emailed to the following:

Board of Finance and Revenue

1101 South Front Street

Suite 400

Harrisburg, PA

Phone: (717)

Fax: (717)

bfr@patreasury.gov

Department of Revenue

Attn: BFR Matter

Ofice of Chief Counsel

327 Walnut Street, 10th Floor

P.O. Box 281061

Harrisburg, PA

Phone: (717)

Fax: (717)

Note: Petitions of 20 pages or less do not need to be provided to the Department of Revenue.

Board of Finance & Revenue

Speciic Instructions by Section Number

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

AN E |

A |

N |

|

|

|

|

|

N |

||||

|

|

|

I |

|

|

|

||

|

|

|

F |

|

|

|

|

D |

|

|

O |

F |

|

|

|

|

R |

|

|

|

|

|

|

|

V |

|

|

|

|

|

|

|

|

|

E |

R |

D |

|

|

|

|

|

|

E |

A |

|

|

|

|

|

|

|

N |

O |

|

|

|

|

|

|

|

U |

B |

|

|

|

|

|

|

|

E |

|

|

P |

|

|

|

|

IA |

|

|

|

|

E |

N |

|

|

|

|

|

|

|

|

|

|

N |

||

|

|

|

|

|

NS YLVA |

|||

Each number of the following instructions corresponds to the number of the appropriate section of the petition form. Complete all information applicable to your case.

1.Include the Board of Appeals Docket Number if available.

2.Complete all information. If Petitioner is not an individual, include a contact person.

3.Completed only if Petitioner intends to be represented by another. If so, all correspondence will be sent to the representative.

4.Complete all information, including the tax amount you are appealing. Check one of the two blocks indicating type of petition.

5.Hearings, if requested, are held in Harrisburg and via a

If Petitioner wishes to request a compromise, check the compromise box and complete/ile the

Request for Compromise Form located at www.patreasury.gov/bfrassets/pdf/CompromiseForm.pdf within 30 days of iling the petition.

If the determination of the issue(s) involved in a Petitioner's case would be governed by the decision

of a case pending before a court, the Petitioner may request that its case be continued until the court renders a inal decision. After the court renders a inal decision, the Petitioner's case will be listed for hearing or decided on the record within six months.

6.All petitions must be signed by Petitioner or an authorized representative.

7.Briely list relief requested and basis for relief.

a.The petition must contain a statement of all pertinent facts and/or points of law upon which the Petitioner relies. Calculations showing the proper amount of tax or refund should be supplied.

All evidence in support of the arguments set forth should be submitted with the petition or within 60 days from the date the petition is iled. Late submissions may not be considered by the Board.

b.Explain in detail why the relief requested should be granted. Attach a copy of the notice being appealed (usually the BOA Decision). Petitions for Refund must be accompanied by proof of payment. When appealing sales and use tax, if possible include a copy of the audit, assessment and a

Board of Finance & Revenue

Petition Form

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

AN E |

A |

N |

|

|

|

|

|

N |

||||

|

|

|

I |

|

|

|

||

|

|

|

F |

|

|

|

|

D |

|

|

O |

F |

|

|

|

|

R |

|

|

|

|

|

|

|

V |

|

|

|

|

|

|

|

|

|

E |

R |

D |

|

|

|

|

|

|

E |

A |

|

|

|

|

|

|

|

N |

O |

|

|

|

|

|

|

|

U |

B |

|

|

|

|

|

|

|

E |

|

|

P |

|

|

|

|

IA |

|

|

|

|

E |

N |

|

|

|

|

|

|

|

|

|

|

N |

||

|

|

|

|

|

NS YLVA |

|||

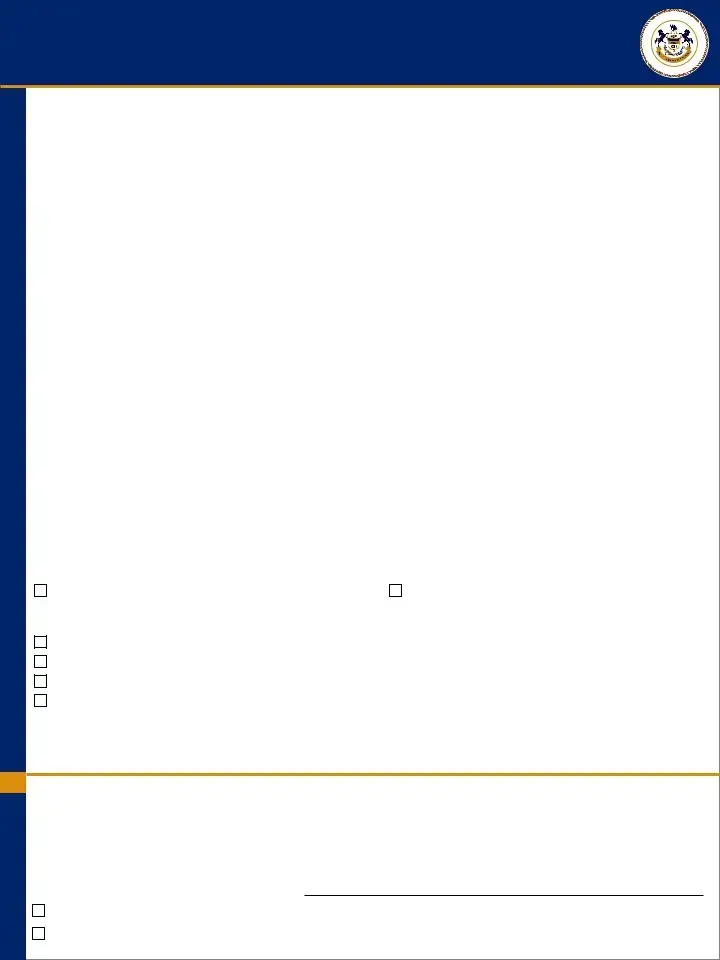

1 |

BOARD OF APPEALS DOCKET NUMBER(S) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DOCKET NUMBER |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

PETITIONER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME OF PETITIONER |

|

|

|

|

|

|

CONTACT PERSON |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

CITY |

|

|

|

|

|

|

|

STATE |

|

ZIP |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TELEPHONE NUMBER |

FAX NUMBER |

|

|

|

|

EMAIL ADDRESS |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

REPRESENTATIVE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME OF REPRESENTATIVE / CONTACT PERSON |

|

NAME OF ORGANIZATION / FIRM |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

CITY |

|

|

|

|

|

|

|

STATE |

|

ZIP |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TELEPHONE NUMBER |

FAX NUMBER |

|

|

|

|

EMAIL ADDRESS |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

TAX TYPE AT ISSUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAX TYPE |

|

|

|

|

|

|

|

|

|

TAX PERIOD START |

TAX PERIOD END |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAXPAYER IDENTIFICATION NUMBER |

ASSESSMENT NUMBER |

|

|

|

|

|

|

|

|

TAX AMOUNT |

|

|

|

||||||

|

|

E.G.(SSN, EIN, ACCT. #) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Review of Resettlement / Reassessment Petition |

|

|

|

|

|

Review of Refund Petition |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

SCHEDULING |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

HEARING DESIRED. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NO HEARING DESIRED. Please decide on the basis of petition and submission(s). |

|

|

|

||||||||||||||

|

|

|

REQUEST FOR COMPROMISE. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

THIS CASE IS REQUESTED TO BE HELD PENDING ACTION OF THE COURT ON THE SAME ISSUE(S). |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CASE NAME |

|

|

|

|

|

COURT CITATION |

|

|

|

||||||||||

6SIGNATURES All petitions must be signed by Petitioner or an authorized representative.

AFFIDAVIT

Under penalties prescribed by law, I hereby afirm that this petition has been examined by me and to the best of my

knowledge, information and belief, is true and correct and is not made for the purpose of delay. Also, if this is a petition for a cash refund, I further afirm that all taxes have been paid to the Commonwealth and there are no outstanding tax liabilities.

Please check one:

PETITIONER |

SIGNATURE |

|

|

|

|

|

|

AUTHORIZED REPRESENTATIVE |

|

|

|

|

PRINT NAME |

DATE |

|

Board of Finance & Revenue

Petition Form

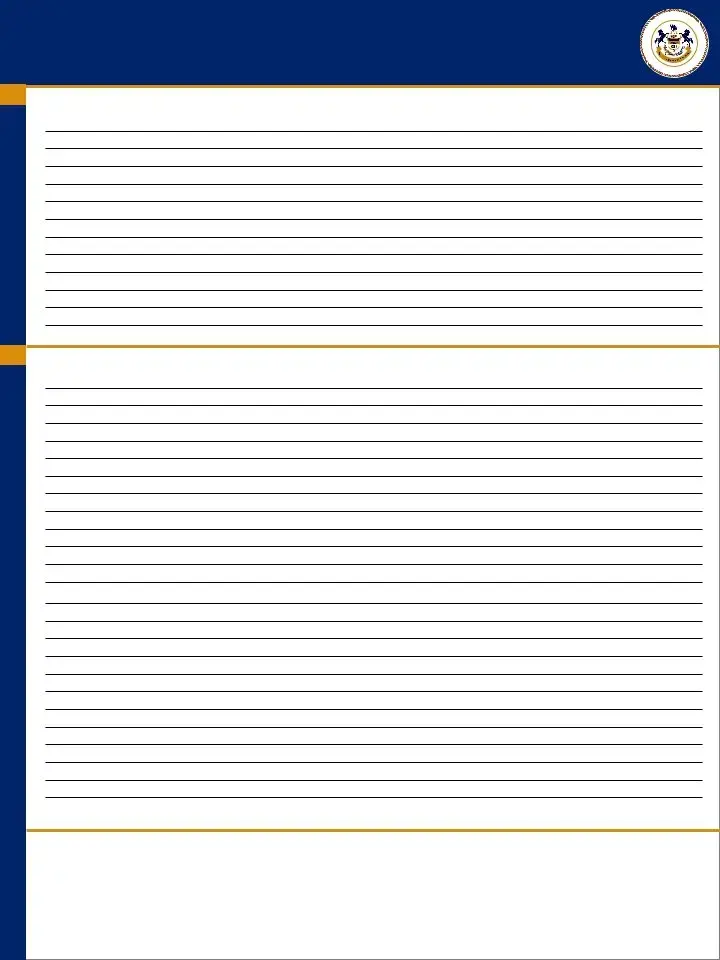

7A RELIEF REQUESTED:

7B ARGUMENTS:

FOR PAPER SUBMISSION(S): |

FOR ELECTRONIC SUBMISSION(S): |

|

Board of Finance and Revenue |

Email: bfr@patreasury.gov |

|

1101 South Front Street, Suite 400 |

Fax: 717.783.4499 |

|

Harrisburg, PA |

||

Phone: 717.787.2974 |

||

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

AN E |

A |

N |

|

|

|

|

|

N |

||||

|

|

|

I |

|

|

|

||

|

|

|

F |

|

|

|

|

D |

|

|

O |

F |

|

|

|

|

R |

|

|

|

|

|

|

|

V |

|

|

|

|

|

|

|

|

|

E |

R |

D |

|

|

|

|

|

|

E |

A |

|

|

|

|

|

|

|

N |

O |

|

|

|

|

|

|

|

U |

B |

|

|

|

|

|

|

|

E |

|

|

P |

|

|

|

|

IA |

|

|

|

|

E |

N |

|

|

|

|

|

|

|

|

|

|

N |

||

|

|

|

|

|

NS YLVA |

|||

| Fact Name | Description |

|---|---|

| Purpose of the Petition | This form is used to petition the Board of Finance and Revenue for a review of decisions made by the Board of Appeals or to request a refund of payments made to a Commonwealth agency. |

| Submission Guidelines | Petitioners must submit any supporting evidence either with the petition or within 60 days of filing. Electronic submissions are preferred, with a maximum size of 10MB. |

| Petitioner's Responsibilities | Both the petitioner and the Department of Revenue must provide copies of all submissions to each other. This ensures transparency and effective communication throughout the process. |

| Hearing Information | Hearings, if requested, will be held in Harrisburg or via video conference from Pittsburgh. The petitioner will receive notice of the hearing date. |

| Required Signatures | All petitions must be signed by the petitioner or an authorized representative. This ensures accountability and compliance with legal standards. |

| Governing Law | The petition process is governed by Pennsylvania law, specifically the regulations set forth by the Board of Finance and Revenue. |